the zero lower bound remains a medium term risk

cent·@darkflame·

0.388 HBDthe zero lower bound remains a medium term risk

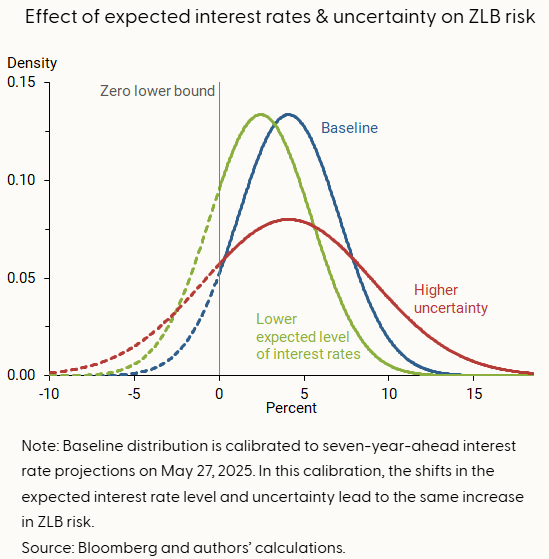

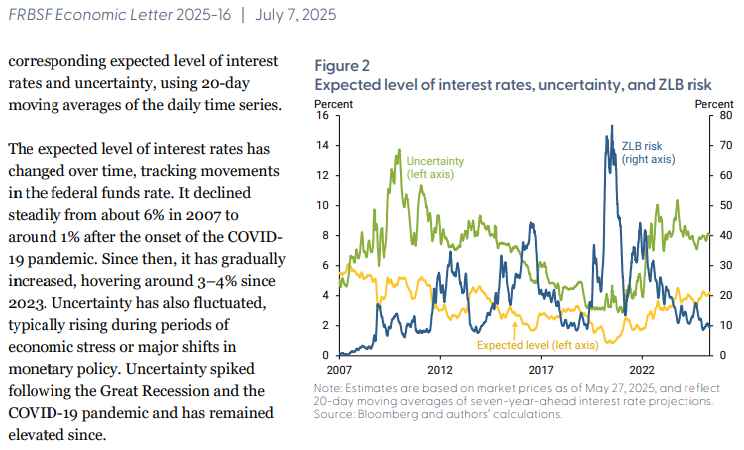

Here is an interesting article that I discovered. ---------------  #### <u>Authors:</u> Sophia Cho, Thomas Mertens, John C. Williams > "Financial market derivatives provide real-time forward-looking measures of the perceived risk of reaching the zero lower bound in the future. This ZLB risk tends to fall with higher expected levels of interest rates and tends to rise with interest rate uncertainty. Compared with the past decade, current data show that expected levels of future interest rates are high. Nevertheless, ZLB risk remains significant over the medium to long term, similar to levels observed in 2018, due to recent elevated uncertainty." https://www.frbsf.org/research-and-insights/publications/economic-letter/2025/07/zero-lower-bound-remains-medium-term-risk/  PDF -> https://www.frbsf.org/wp-content/uploads/el2025-16.pdf  > "With an expected level of interest rates around 3–4%, the perceived risk of returning to the ZLB over the next two years is about 1%. This risk increases to about 9% at the seven-year horizon and remains at similar levels over longer horizons. To put the current term structure into context, medium- to long-term ZLB risk is currently at the lower end of the range observed over the past 15 years. The last time seven-year-ahead ZLB risk reached a similar level was in 2018. But the composition of ZLB risk has changed since then: While the expected level of interest rates at the seven-year horizon is about a full percentage point higher than in 2018, the current considerably elevated uncertainty offsets it and results in a comparable likelihood of reaching the ZLB. Updates related to the term structure of ZLB risk and the time series for different horizons are available on the San Francisco Fed’s <a href="https://www.frbsf.org/research-and-insights/data-and-indicators/zero-lower-bound-probabilities-at-different-time-horizons/">Zero Lower Bound Probabilities</a> data page (<a href="https://archive.is/VIHtp">archived</a>)." --------------- #### Here is the Archived web page article. https://archive.is/Hevb5

👍 darkflame, sciencevienna, yourfuture, freebornsociety, mochita, condigital, zuun.net, neoxianvoter, auracraft, darkpylon, xchng, plusvault, tomwafula, minerspost, patronpass, steem-holder, arrrds, sidekicker2, neoxvoter, pixelfan, cconn, leoball, grapthar, da-dawn, dylanhobalart, magic.bee, mirroredspork, favouragina, trezzahn, fat-elvis, nave7, politicalhive,